If you're new to home loans, mortgage insurance is one of those terms that tends to cause confusion. Knowing a few key facts about how it works can help you make a smarter financial decision and avoid surprises when you're going through the process.

Mortgage insurance defined

Mortgage insurance can be a great way to get into a home if you have less than 20% to put down when you take out a home loan. But instead of protecting your home, mortgage insurance protects your lender in case you default on your loan.

Here’s how it works: if you have less than 20% to put down on a home, your lender may see you as a risky borrower. As a way to protect themselves and their investors while still making the loan, lenders require you to pay mortgage insurance.

This insurance comes in two varieties: private mortgage insurance (PMI) and mortgage insurance premiums (MIP). PMI is primarily for conventional loans, and you pay it every month as part of your mortgage payment. MIP is for FHA loans, and you pay a premium at closing in addition to monthly premiums with your mortgage payment.

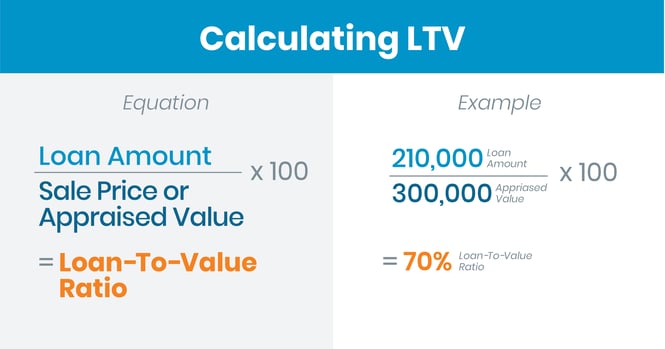

Another acronym gets thrown around a lot when mortgage insurance comes up, and that's LTV. It stands for loan-to-value ratio, and it refers to the portion of your home you own compared to how much your lender owns. If you had 20% to put down when you took out the loan, your LTV would have been 80%. That figure drops as the value of your home increases and you make payments toward the total amount borrowed.

How to drop mortgage insurance

Mortgage insurance costs differ depending on the type of loan you get, but average costs are between 0.5% and 1.5% of your total loan amount each year. For a $350,000 home, that would amount to between $1,750 and $5,250.

That’s a big chunk of change for a lot of families, but it doesn’t have to be a permanent cost of homeownership. Depending on your loan type, you can either drop it automatically or refinance into a new loan when your LTV is low enough.

Conventional loans

With this type of loan, it’s possible to simply request cancelation of your PMI once your LTV is less than 80%. If you don't make that request, the mortgage insurance will drop off automatically if your balance reaches 78% of the original value of the home or you reach the middle of your mortgage term—whichever comes first.

For that drop off to occur, you’ll need to be current on payments, have no additional liens, and your home can’t have decreased in value.

FHA loans

If your FHA loan started after June of 2013 and you had an LTV of 90% or more, you’ll need to pay mortgage insurance for the life of the loan. If your loan started before that time with that same 90% LTV, the mortgage insurance will automatically drop off after 11 years.

USDA loans

If you bought a home in a rural area using a USDA loan, you will need to pay mortgage insurance for the life of the loan. However, it may make sense to refinance when your LTV drops below 80%. Your loan officer can explain all the details.

VA loans

One of the benefits for current and former service members who utilize VA loans is that mortgage insurance is never required. However, you will be required to pay a funding fee when you first take out the loan.

The case for mortgage insurance

Some buyers avoid getting into homes because they don't want to pay mortgage insurance. But it's worth doing the math before you write it off.

Here's a simple example. Say you have a $12,250 down payment on a $350,000 home. Your LTV would be 96.5%, and you'd pay mortgage insurance. At 1% of the loan value per year, that's $3,500 annually on top of your regular mortgage payment.

That feels like a lot, until you consider what you're getting in return.

Home values tend to increase over time. As your home appreciates and you continue making payments, your equity grows. Within a few years, many homeowners find themselves with significantly more equity than the total amount they paid in mortgage insurance. For some buyers, paying mortgage insurance could be the move that gets them into a home and building wealth years earlier than waiting to save a full 20% down payment would have.

Have questions about mortgage insurance?

Your Castle & Cooke Mortgage loan officer can walk you through your down payment options, explain which type of mortgage insurance applies to your loan, and help you understand exactly what it will cost and when you can drop it.